I gave a guest lecture at Birkbeck College, of the University of London on the evening of 22nd February 2017 in the evening, as part of the Energy and Climate Change module. I titled it, “Renewable Gas for Energy Storage : Scaling up the ‘Gas Battery’ to balance Wind and Solar Power and provide Low Carbon Heat and Transport”.

The basic concept is that since wind and solar power are variable in output, there has to be some support from other energy technologies. Some talk of batteries to store electrical energy as a chemical potential, and when they talk of batteries they think of large Lithium ion piles, or flow batteries, or other forms of liquid electrolyte with cathodes and anodes. When I talk about batteries, I think of electrical energy stored in the form of a gas. This gas battery doesn’t need expensive metal cathodes or anodes, and it doesn’t need an acid liquid electrolyte to operate. Gas that is synthesised from excess solar or wind power can be a fuel that can be used in chemical reactions, such as combustion, or burning, to generate electricity and heat when desired at some point in the future. It could be burned in a gas turbine, a gas boiler or a fuel cell, or in a vehicle engine. Or instead, a chemically inert gas can be stored under pressure, and this compressed gas can also be used to generate power on demand at a later date by harnessing energy from decompression. Another option would be holding a chemically reactive gas under pressure, allowing two stages of energy recovery.

As expected, the Birkbeck audience was very diverse, and had different social and educational backgrounds, and so there was little that could be assumed as common knowledge, especially since the topic was energy, which is normally only an interest for engineers, or at a stretch, economists.

I decided when preparing that I would attempt to use symbolism as a tool to build a narrative in the presentation. A bold move, perhaps, but I found it created an emblematic thread that ran through the slides quite nicely, and helped me tell the story. I used Mathematical and Physical notation, but I didn’t do any Mathematics or Physics.

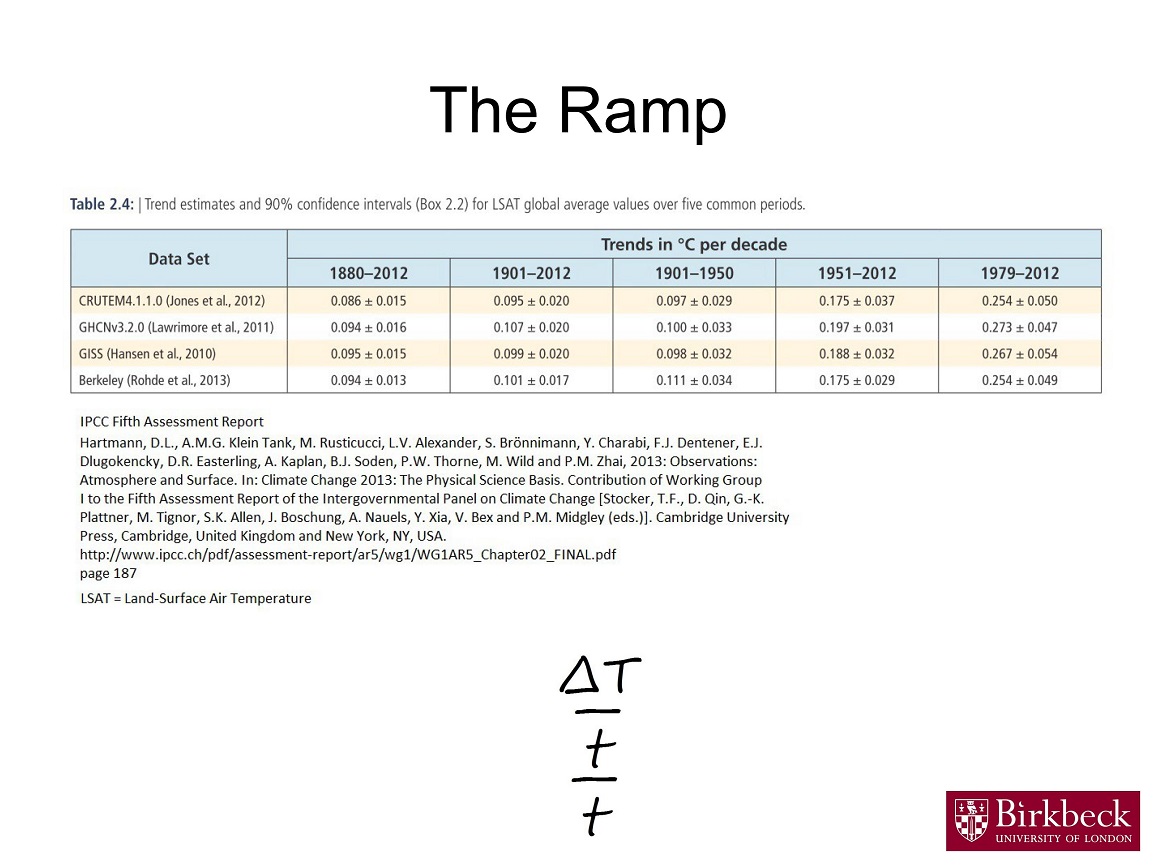

I introduced the first concept : the Delta, or change. I explained this delta was not the same as a river delta, which gave me the excuse to show a fabulous night sky image of the Nile Delta taken from the International Space Station. I demonstrated the triangle shape that emerges from charting data that changes over time, and calculating its gradient, such as the temperature of the Earth’s surface.

I explained that the change in temperature of the Earth’s surface over the recent decades is an important metric to consider, not just in terms of scale, but in terms of speed. I showed that this rate of change appears in all the independent data sets.

I then went on to explain that the overall trend in the change in the temperature of the Earth’s surface is not the only phenomenon. Within regions, and within years and seasons, even between months and days, there are smaller scale changes that may not look like the overall delta. A lot of these changes give the appearance of cyclic phenomena, and they can have a periodicity of up to several decades, for example, “oscillations” in the oceans.

These discrete deltas and cycles could, to a casual observer, mask underlying trends, especially as the deltas can be larger than the trends; so climatologists look at a large set of measurements of all kinds, and have shown that some deltas are one way only, and are not cycling.

Teasing out the trends in all of the observations is a major enterprise that has been accomplished by thousands of scientists who have reported to the IPCC, the Intergovernmental Panel on Climate Change, part of the UNFCCC, the United Nations Framework Convention on Climate Change. The Fifth Assessment Report is the most comprehensive yet, and shows that global warming is almost certainly ramping up – in other words, global warming is getting faster, or accelerating.

Many projections for the future of temperature changes at the Earth’s surface have been done, with the overall view that temperatures are likely to carry on rising for hundreds of years without an aggressive approach to curtail net greenhouse gas emissions to the atmosphere – principally carbon dioxide (CO2), methane (CH4) and nitrous oxide (N2O).

From observations, it is clear that global warming causes climate change, and that the rate of temperature change is linked to the rate of climate change. In symbols, this reads : delta T for temperature over t for time leads to, or implies, a delta C for climate over t for time. The fact that global warming and its consequential climate change are able to continue worsening under the current emissions profile means that climate change is going to affect humanity for a long stretch. It also means that efforts to rein in emissions will also need to extend over time.

I finished this first section of my presentation by showing a list of what I call “Solution Principles” :-

1. Delays embed and extend the problem, making it harder to solve. So don’t delay.

2. Solve the problem at least as fast as creating it.

3. For maximum efficiency, minimum cost, and maximum speed, re-deploy agents of the problem in its solution.

In other words, make use of the existing energy, transport, agriculture, construction and chemical industries in approaching answers to the imperative to address global warming and climate change.

In my seemingly futile and interminable quest to reconcile the differences between the data provided by the JODI Oil organisation and BP as revealed in part by the annual BP Statistical Review of World Energy, I have moved on to looking at production (primary supply), found a problem as regards Africa, and had some confirmation that a major adjustment in how the data is collected happened in 2009.

First – the problem with Africa. The basket “Other Africa” for oil production is far less in the BP data than it is in the JODI Oil data – shown by negative figures in the comparison. For 2015, this is approximately 65% in scale (-3800 KBD) of the summed positive difference between the BP and JODI figures for the named countries (5884 KBD). This reminds me that there was a problem with the refined oil product consumption figures for “Other Africa” as well. Without a detailed breakdown of individual country accounts from BP it is almost impossible to know where these differences arise, it seems to me, or begin to understand why these differences are so large. Maybe I should just ask BP for a full country breakdown – if they’d ever deign to communicate this kind of information with me. Standing by my email Inbox right now… Could be here some time…

It is fairly clear from the comparison for North America that a major shift in understanding by either BP or JODI Oil took place in 2009, as the oil production data converge significantly for that year onwards. There was similar evidence of this in the refined oil products consumption data.

As with the consumption data, the production data for the Middle East region is strongly divergent between BP and JODI. I did read something potentially useful in the JODI Oil Manual, which I would recommend everyone interested in energy data to read. In the notes for Crude Oil, I read : “One critical issue is whether the volumes of NGL, lease or field condensates and oils extracted from bituminous minerals are included. All organisations exclude NGL from crude oil. If condensates are able to be excluded, it should be noted to the JODI organisation(s) of which the country/economy is a member. Most OPEC member countries exclude condensates.” Now, I guess, the struggle will be to find some data on condensates. Of which there are a variety of sources and nomenclature, be they light liquid hydrocarbons from oil and gas production or oil and gas refining/processing/cryoprocessing. There may be faultlines of comprehension and categorisation, such as about who considers NGPL or Natural Gas Plant Liquids from Natural Gas processing plants to be in the category of NGLs – Natural Gas Liquids, and therefore effectively in the bucket of Crude Oil.

I’m no closer to any answers on why BP oil data doesn’t align with JODI Oil data. And it looks like I’ve just opened a whole can of condensate wormy questions.

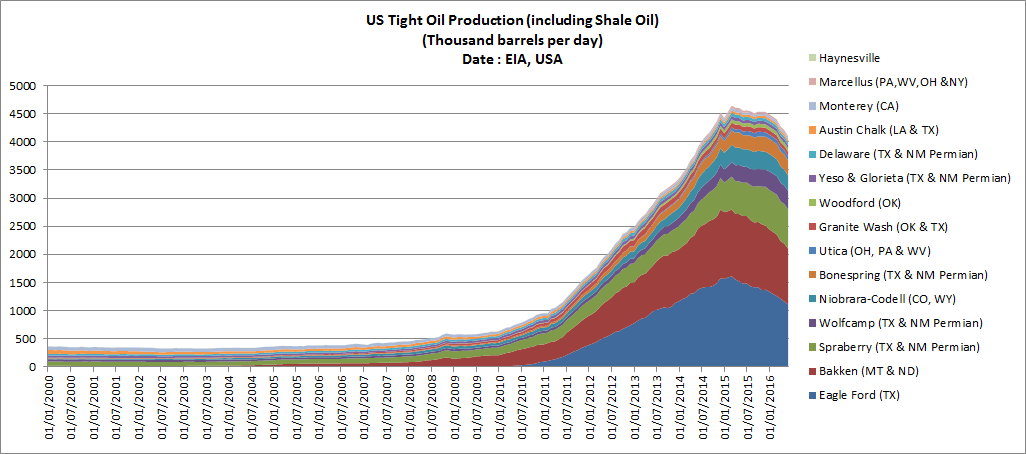

Peak conventional crude petroleum oil production is apparently here already – the only thing that’s been growing global total liquids is North American unconventional oils : tight oil – which includes shale oil in the United States of America – and tar sands oil from bitumen in Canada – either refined into synthetic crude, or blended with other oils – both heavy and light.

But there’s a problem with unconventional oils – or rather several – but the key one is the commodity price of oil, which has been low for many months, and has caused unconventional oil producers to rein in their operations. It’s hitting conventional producers too. A quick check of Section 3 “Oil data : upstream” in OPEC’s 2016 Annual Statistical Bulletin shows a worrying number of negative 2014 to 2015 change values – for example “Active rigs by country”, “Wells completed in OPEC Members”, and “Producing wells in OPEC Members”.

But in the short term, it’s the loss of uneconomic unconventional oil production that will hit hardest. Besides problems with operational margins for all forms of unconventionals, exceptional air temperatures (should we mention global warming yet ?) in the northern part of North America have contributed to a seizure in Canadian tar sands oil production – because of extensive wildfires.

Here’s two charted summaries of the most recent data from the EIA on tight oil (which includes shale oil) and dry shale gas production in the United States – which is also suffering.

Once the drop in North American unconventionals begins to register in statistics for global total liquids production, some concern will probably be expressed. Peak Oil just might be sharper and harder and sooner than some people think.

Our assiduous government in the United Kingdom has conducted a national security review, as they should, but it appears the collective intelligence on energy of the Prime Minister’s office, the Cabinet Office and the Foreign Commonwealth Office is on a scale of poor to dangerously out of date.

No, LNG doesn’t stand for “liquid natural gas”. LNG stands for Liquefied Natural Gas. I think this report has confused LNG with NGLs.

Natural Gas Liquids, or NGLs, are condensable constituents of gas-prone hydrocarbon wells. In other words, the well in question produces a lot of gas, but at the temperatures and pressures in the well underground, hydrocarbons that would normally be liquid on the surface are in the gas phase, underground. But when they are pumped/drilled out, they are condensed to liquids. So, what are these chemicals ? Well, here are the approximate Boiling Points of various typical fossil hydrocarbons, approximate because some of these molecules have different shapes and arrangements which influences their physical properties :-

Boiling Points of Short-Chain Hydrocarbons

Methane : approximately -161.5 degrees Celsius

Ethane : approximately -89.0 degrees Celsius

Propane : approximattely -42.0 degrees Celsius

Butane : approximately -1.0 degrees Celsius

Pentane : approximately 36.1 degrees Celsius

Heptane : approximately 98.42 degrees Celsius

You would expect NGLs, liquids condensed out of Natural Gas, to be mostly butane and heavier molecules, but depending on the techniques used – which are often cryogenic – some propane and ethane can turn up in NGLs, especially if they are kept cold. The remaining methane together with small amounts of ethane and propane and a trace of higher hydrocarbons is considered “dry” Natural Gas.

By contrast, LNG is produced by a process that chills Natural Gas without separating the methane, until it is liquid, and takes up a much smaller volume, making it practical for transportation. OK, you can see why mistakes are possible. Both processes operate at sub-zero temperatures and result in liquid hydrocarbons. But it is really important to keep these concepts separate – especially as methane-free liquid forms of short-chain hydrocarbons are often used for non-energy purposes.

Amongst other criticisms I have of this report, it is important to note that the UK’s production of crude oil and Natural Gas is not “gradually” declining. It is declining at quite a pace, and so imports are “certain” to grow, not merely “likely”. I note that Natural Gas production decline is not mentioned, only oil.

So I met somebody last week, at their invitation, to talk a little bit about my research into Renewable Gas.

I can’t say who it was, as I didn’t get their permission to do so. I can probably (caveat emptor) safely say that they are a fairly significant player in the energy engineering sector.

I think they were trying to assess whether my work was a bankable asset yet, but I think they quickly realised that I am nowhere near a full proposal for a Renewable Gas system.

Although there were some technologies and options over which we had a meeting of minds, I was quite disappointed by their opinions in connection with a number of energy projects in the United Kingdom.

Out of the blue, I got an invitation to a meeting in Whitehall.

I was to join industrial developers and academic researchers at the Department of Energy and Climate Change (DECC) in a meeting of the “Green Hydrogen Standard Working Group”.

The date was 12th June 2015. The weather was sunny and hot and merited a fine Italian lemonade, fizzing with carbon dioxide. The venue was an air-conditioned grey bunker, but it wasn’t an unfriendly dungeon, particularly as I already knew about half the people in the room.

The subject of the get-together was Green Hydrogen, and the work of the group is to formulate a policy for a Green Hydrogen standard, navigating a number of issues, including the intersection with other policy, and drawing in a very wide range of chemical engineers in the private sector.

My reputation for not putting up with any piffle clearly preceded me, as somebody at the meeting said he expected I would be quite critical. I said that I would not be saying anything, but that I would be listening carefully. Having said I wouldn’t speak, I must admit I laughed at all the right places in the discussion, and wrote copious notes, and participated frequently in the way of non-verbal communication, so as usual, I was very present. At the end I was asked for my opinion about the group’s work and I was politely congratulational on progress.

So, good. I behaved myself. And I got invited back for the next meeting. But what was it all about ?

Most of what it is necessary to communicate is that at the current time, most hydrogen production is either accidental output from the chemical industry, or made from fossil fuels – the main two being coal and Natural Gas.

Hydrogen is used extensively in the petroleum refinery industry, but there are bold plans to bring hydrogen to transport mobility through a variety of applications, for example, hydrogen for fuel cell vehicles.

Clearly, the Green Hydrogen standard has to be such that it lowers the bar on carbon dioxide (CO2) emissions – and it could turn out that the consensus converges on any technologies that have a net CO2 emissions profile lower than steam methane reforming (SMR), or the steam reforming of methane (SRM), of Natural Gas.

[ It’s at this very moment that I need to point out the “acronym conflict” in the use of “SMR” – which is confusingly being also used for “Small Modular Reactors” of the nuclear fission kind. In the context of what I am writing here, though, it is used in the context of turning methane into syngas – a product high in hydrogen content. ]

Some numbers about Carbon Capture and Storage (CCS) used in the manufacture of hydrogen were presented in the meeting, including the impact this would have on CO2 emissions, and these were very intriguing.

I had some good and useful conversations with people before and after the meeting, and left thinking that this process is going to be very useful to engage with – a kind of dragnet pulling key players into low carbon gas production.

Here follow my notes from the meeting. They are, of course, not to be taken verbatim. I have permission to recount aspects of the discussion, in gist, as it was an industrial liaison group, not an internal DECC meeting. However, I should not say who said what, or which companies or organisations they are working with or for.

As if to provide proof for the sneaking suspicion that Great Britain is run by the wealthy, rather than by the people, and that energy policy is decided by a close-knit circle of privileged dynasties, up bubbles Amber Rudd MP’s first whirl of skirmish as Secretary of State for Energy and Climate Change : her brother Roland is chairperson of a lobbying firm, Finsbury, which is seeking to get state approval for a controversial gas storage scheme at Preesall, near Fleetwood, on behalf of the developers, Halite Energy of Preston, Lancashire.

Whilst some claim there is a starkly obvious conflict of interest for Rudd to take part in the decision-making process, the Department of Energy and Climate Change (DECC) could have denied it, but have instead confirmed that the potential reversal of a 2013 decision will be made, not by Rudd, but by Lord Bourne.

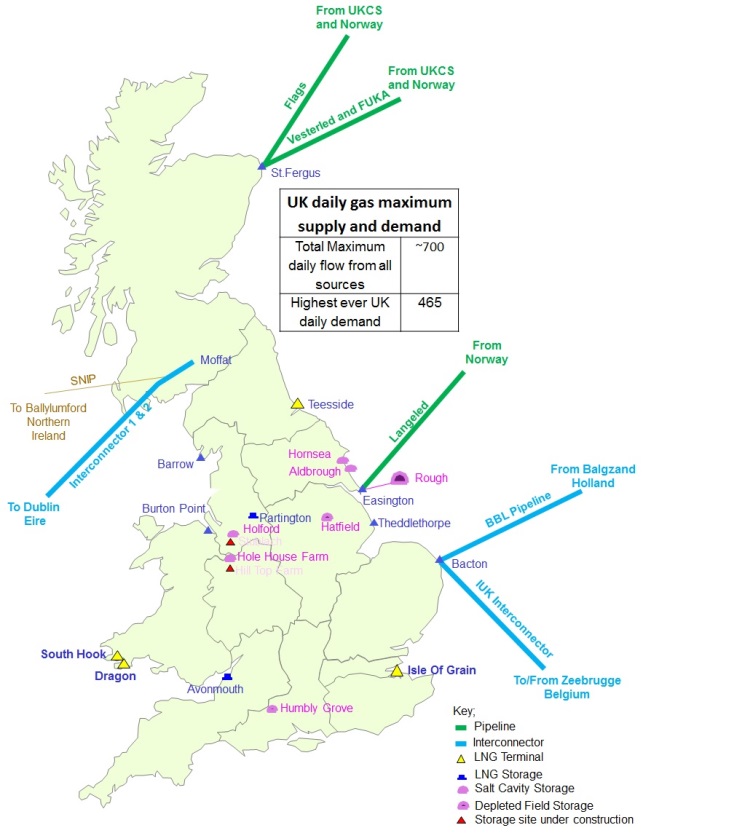

New gas storage in the United Kingdom is a crucial piece of the energy infrastructure provision, as recognised by successive governments. Developments have been ongoing, such as the opening of the Holford facility at Byley in Cheshire. Besides new gas storage, there are anticipated improvements for interconnectors with mainland Europe. These are needed for raising the volume of Natural Gas available to the British market, and for optimising Natural Gas flows and sales in the European regional context – a part of the EC’s “Energy Union”.

An underlying issue not much aired is that increased gas infrastructure is necessary not just to improve competition in the energy markets – it is also to compensate for Peak Natural Gas in the North Sea – something many commentators regularly strive to deny. The new Conservative Government policy on energy is not fit to meet this challenge. The new Secretary of State has gone public about the UK Government’s continued commitment to the exploitation of shale gas – a resource that even her own experts can tell her is unlikely to produce more than a footnote to annual gas supplies for several decades. In addition, should David Cameron be forced to usher in a Referendum on Europe, and the voters petulantly pull out of the Europe project, Britain’s control over Natural Gas imports is likely to suffer, either because of the failure of the “Energy Union” in markets and infrastructure, or because of cost perturbations.

Amber Rudd MP is sitting on a mountain of trouble, undergirded by energy policy vapourware : the promotion of shale gas is not going to solve Britain’s gas import surge; the devotion to new nuclear power is not going to bring new atomic electrons to the grid for decades, and the UK Continental Shelf is going to be expensive for the Treasury to incentivise to mine. What Amber needs is a proper energy policy, based on focused support for low carbon technologies, such as wind power, solar power and Renewable Gas to back up renewable electricity when the sun is not shining and wind is not blowing.

Volatile crude petroleum oil commodity prices over the last decade have played some undoubted havoc with oil and gas company strategy. High crude prices have pushed the choice of refinery feedstocks towards cheap heavy and immature gunk; influenced decisions about the choices for new petrorefineries and caused ripples of panic amongst trade and transport chiefs : you can’t keep the engine of globalisation ticking over if the key fuel is getting considerably more expensive, and you can’t meet your carbon budgets without restricting supplies.

Low crude commodity prices have surely caused oil and gas corporation leaders to break out into the proverbial sweat. Heavy oil, deep oil, and complicated oil suddenly become unprofitable to mine, drill and pump. Because the economic balance of refinery shifts. Because low commodity prices must translate into low end user refined product prices.

There maybe isn’t an ideal commodity price for crude oil. All the while, as crude oil commodity prices jump around like a medieval flea, the price of Natural Gas, and the gassy “light ends” of slightly unconventional and deep crude oil, stay quite cheap to produce and cheap to use. It’s a shame that there are so many vehicles on the road/sea/rails that use liquid fuels…all this is very likely to change.

Shell appear to be consolidating their future gas business by buying out the competition. Hurrah for common sense ! The next stage of their evolution, after the transition of all oil applications to gas, will be to ramp up Renewable Gas production : low carbon gas supplies will decarbonise every part of the economy, from power generation, to transport, to heating, to industrial chemistry.

This is a viable low carbon solution – to accelerate the use of renewable electricity – wind power and solar principally – and at the same time, transition the oil and gas companies to become gas companies, and thence to Renewable Gas companies.

In the last couple of years I have researched and written a book about the technologies and systems of Renewable Gas – gas energy fuels that are low in net carbon dioxide emissions. From what I have learned so far, it seems that another energy world is possible, and that the transition is already happening. The forces that are shaping this change are not just climate or environmental policy, or concerns about energy security. Renewable Gas is inevitable because of a range of geological, economic and industrial reasons.

I didn’t train as a chemist or chemical process engineer, and I haven’t had a background in the fossil fuel energy industry, so I’ve had to look at a number of very basic areas of engineering, for example, the distillation and fractionation of crude petroleum oil, petroleum refinery, gas processing, and the thermodynamics of gas chemistry in industrial-scale reactors. Why did I need to look at the fossil fuel industry and the petrochemical industry when I was researching Renewable Gas ? Because that’s where a lot of the change can come from. Renewable Gas is partly about biogas, but it’s also about industrial gas processes, and a lot of them are used in the petrorefinery and chemicals sectors.

In addition, I researched energy system technologies. Whilst assessing the potential for efficiency gains in energy systems through the use of Renewable Electricity and Renewable Gas, I rekindled an interest in fuel cells. For the first time in a long time, I began to want to build something – a solid oxide fuel cell which switches mode to an electrolysis unit that produces hydrogen from water. Whether I ever get to do that is still a question, but it shows how involved I’m feeling that I want to roll up my sleeves and get my hands dirty.

Even though I have covered a lot of ground, I feel I’m only just getting started, as there is a lot more that I need to research and document. At the same time, I feel that I don’t have enough data, and that it will be hard to get the data I need, partly because of proprietary issues, where energy and engineering companies are protective of developments, particularly as regards actual numbers. Merely being a university researcher is probably not going to be sufficient. I would probably need to be an official within a government agency, or an industry institute, in order to be permitted to reach in to more detail about the potential for Renewable Gas. But there are problems with these possible avenues.

You see, having done the research I have conducted so far, I am even more scornful of government energy policy than I was previously, especially because of industrial tampering. In addition, I am even more scathing about the energy industry “playing both sides” on climate change. Even though there are some smart and competent people in them, the governments do not appear to be intelligent enough to see through expensive diversions in technology or unworkable proposals for economic tweaking. These non-solutions are embraced and promoted by the energy industry, and make progress difficult. No, carbon dioxide emissions taxation or pricing, or a market in carbon, are not going to make the kind of changes we need on climate change; and in addition they are going to be extremely difficult and slow to implement. No, Carbon Capture and Storage, or CCS, is never going to become relatively affordable in any economic scenario. No, nuclear power is too cumbersome, slow and dodgy – a technical term – to ever make a genuine impact on the total of carbon emissons. No, it’s not energy users who need to reduce their consumption of energy, it’s the energy companies who need to reduce the levels of fossil fuels they utilise in the energy they sell. No, unconventional fossil fuels, such as shale gas, are not the answer to high emissions from coal. No, biofuels added to petrofuels for vehicles won’t stem total vehicle emissions without reducing fuel consumption and limiting the number of vehicles in use.

I think that the fossil fuel companies know these proposals cannot bring about significant change, which is precisely why they lobby for them. They used to deny climate change outright, because it spelled the end of their industry. Now they promote scepticism about the risks of climate change, whilst at the same time putting their name to things that can’t work to suppress major amounts of emissions. This is a delayer’s game.

Because I find the UK Government energy and climate policy ridiculous on many counts, I doubt they will ever want me to lead with Renewable Gas on one of their projects. And because I think the energy industry needs to accept and admit that they need to undergo a major change, and yet they spend most of their public relations euros telling the world they don’t need to, and that other people need to make change instead, I doubt the energy industry will ever invite me to consult with them on how to make the Energy Transition.

I suppose there is an outside chance that the major engineering firms might work with me, after all, I have been an engineer, and many of these companies are already working in the Renewable Gas field, although they’re normally “third party” players for the most part – providing engineering solutions to energy companies.

Because I’ve had to drag myself through the equivalent of a “petro degree”, learning about the geology and chemistry of oil and gas, I can see more clearly than before that the fossil fuel industry contains within it the seeds of positive change, with its use of technologies appropriate for manufacturing low carbon “surface gas”. I have learned that Renewable Gas would be a logical progression for the oil and gas industry, and also essential to rein in their own carbon emissions from processing cheaper crude oils. If they weren’t so busy telling governments how to tamper with energy markets, pushing the blame for emissions on others, and begging for subsidies for CCS projects, they could instead be planning for a future where they get to stay in business.

The oil and gas companies, especially the vertically integrated tranche, could become producers and retailers of low carbon gas, and take part in a programme for decentralised and efficient energy provision, and maintain their valued contribution to society. At the moment, however, they’re still stuck in the 20th Century.

I’m a positive person, so I’m not going to dwell too much on how stuck-in-the-fossilised-mud the governments and petroindustry are. What I’m aiming to do is start the conversation on how the development of Renewable Gas could displace dirty fossil fuels, and eventually replace the cleaner-but-still-fossil Natural Gas as well.

I was in a meeting today held at the Centre for European Reform in which Shell’s Chief Financial Officer, Simon Henry, made two arguments to absolve the oil and gas industry of responsibility for climate change. He painted coal as the real enemy, and reiterated the longest hand-washing argument in politics – that Shell believes that a Cap and Trade system is the best way to suppress carbon dioxide emissions. In other words, it’s not up to Shell to do anything about carbon. He argued that for transportation and trade the world is going to continue to need highly energy-dense liquid fuels for some time, essentially arguing for the continuation of his company’s current product slate. He did mention proudly in comments after the meeting that Shell are the world’s largest bioethanol producers, in Brazil, but didn’t open up the book on the transition of his whole company to providing the world with low carbon fuels. He said that Shell wants to be a part of the global climate change treaty process, but he gave no indication of what Shell could bring to the table to the negotiations, apart from pushing for carbon trading. Mark Campanale of the Carbon Tracker Initiative was sufficiently convinced by the “we’re not coal” argument to attempt to seek common cause with Simon Henry after the main meeting. It would be useful to have allies in the oil and gas companies on climate change, but it always seems to be that the rest of the world has to adopt Shell’s and BP’s view on everything from policy to energy resources before they’ll play ball.

During the meeting, Mark Campanale pointed out in questions that Deutsche Bank and Goldman Sachs are going to bring Indian coal to trade on the London Stock Exchange and that billions of dollars of coal stocks are to be traded in London, and that this undermines all climate change action. He said he wanted to understand Shell’s position, as the same shareholders that hold coal (shares), hold Shell. I think he was trying to get Simon Henry to call for a separation in investment focus – to show that investment in oil and gas is not the same as investing in Big Bad Coal. But Simon Henry did not bite. According to the Carbon Tracker Initiative’s report of 2013, Unburnable Carbon, coal listed on the London Stock Exchange is equivalent to 49 gigatonnes of Carbon Dioxide (gtCO2), but oil and gas combined trade shares for stocks equivalent to 64 gtCO2, so there’s currently more emissions represented by oil and gas on the LSX than there is for coal. In the future, the emissions held in the coal traded in London have the potential to amount to 165 gtCO2, and oil and gas combined at 125 gtCO2. Despite the fact that the United Kingdom is only responsible for about 1.6% of direct country carbon dioxide emissions (excluding emissions embedded in traded goods and services), the London Stock Exchange is set to be perhaps the world’s third largest exchange for emissions-causing fuels.

Here’s a rough transcript of what Simon Henry said. There are no guarantees that this is verbatim, as my handwriting is worse than a GP’s.

[Simon Henry] I’m going to break the habit of a lifetime and use notes. Building a long-term sustainable energy system – certain forces shaping that. 7 billion people will become 9 billion people – [many] moving from off-grid to on-grid. That will be driven by economic growth. Urbanisation [could offer the possibility of] reducing demand for energy. Most economic growth will be in developing economies. New ways fo consuming energy. Our scenarios – in none do we see energy not growing materially – even with efficiencies. The current ~200 billion barrels of oil equivalent per day today of energy demand will rise to ~400 boe/d by 2050 – 50% higher than today. This will be demand-driven – nothing to do with supply…

[At least one positive-sounding grunt from the meeting – so there are some Peak Oil deniers in the room, then.]

[Simon Henry] …What is paramount for governments – if a threat, then it gets to the top of the agenda. I don’t think anybody seriously disputes climate change…

[A few raised eyebrows and quizzical looks around the table, including mine]

[Simon Henry] …in the absence of ways we change the use of energy […] Any approach to climate change has got to embrace science, policy and technology. All three levers must be pulled. Need a long-term stable policy that enables technology development. We think this is best in a market mechanism. […] Energy must be affordable at the point of use. What we call Triple A – available, acceptable and affordable. No silver bullet. Develop in a responsible way. Too much of it is soundbite – that simplifies what’s not a simple problem. It’s not gas versus coal. [Although, that appeared to be one of his chief arguments – that it is gas versus coal – and this is why we should play nice with Shell.]

1. Economy : About $1.5 to $2 trillion of new money must be invested in the energy industry each year, and this must be sustained until 2035 and beyond. A [few percent] of the world economy. It’s going to take time to make [massive changes]. […] “Better Growth : Better Climate” a report on “The New Climate Economy” by the Global Commission on the Economy and Climate, the Calderon Report. [The world invested] $700 billion last year on oil and gas [or rather, $1 trillion] and $220 – $230 billion on wind power and solar power. The Calderon Report showed that 70% of energy is urban. $6 trillion is being spent on urban infrastructure [each year]. $90 trillion is available. [Urban settings are] more compact, more connected, there’s public transport, [can build in efficiencies] as well as reducing final energy need. Land Use is the other important area – huge impact on carbon emissions. Urbanisation enables efficiency in distributed generation [Combined Heat and Power (CHP)], [local grids]. Eye-popping costs, but the money will be spent anyway. If it’s done right it will [significantly] reduce [carbon emissions and energy demand]…

2. Technology Development : Governments are very bad at picking winners. Better to get the right incentives in and let the market players decide [optimisation]. They can intervene, for example by [supporting] Research and Development. But don’t specify the means to an end…The best solution is a strong predictable carbon price, at $40 a tonne or more or it won’t make any difference. We prefer Cap and Trade. Taxes don’t actually decrease carbon [emissions] but fundamentally add cost to the consumer. As oil prices rose [in 2008 – 2009] North Americans went to smaller cars…Drivers [set] their behaviour from [fuel] prices…

[An important point to note here : one of the reasons why Americans used less motor oil during the “Derivatives Bubble” recession between 2006 and 2010 was because the economy was shot, so people lost their employment, and/or their homes and there was mass migration, so of course there was less commuter driving, less salesman driving, less business driving. This wasn’t just a response to higher oil prices, because the peak in driving miles happened before the main spike in oil prices. In addition, not much of the American fleet of cars overturned in this period, so Americans didn’t go to smaller cars as an adaptation response to high oil prices. They probably turned to smaller cars when buying new cars because they were cheaper. I think Simon Henry is rather mistaken on this. ]

[Simon Henry] …As regards the Carbon Bubble : 65% of the Unburnable fossil fuels to meet the 2 degrees [Celsius] target is coal. People would stuggle to name the top five coal companies [although they find it easy to name the top five oil and gas companies]. Bearing in mind that you have to [continue to] transport stuff [you are going to need oil for some time to come.] Dealing with coal is the best way of moving forward. Coal is used for electricity – but there are better ways to make electricity – petcoke [petroleum coke – a residue from processing heavy and unconventional crude oil] for example…

[The climate change impact of burning (or gasifying) petroleum coke for power generation is possibly worse than burning (or gasifying) hard coal (anthracite), especially if the pet coke is sourced from tar sands, as emissions are made in the production of the pet coke before it even gets combusted.]

[Simon Henry] …It will take us 30 years to get away entirely from coal. Even if we used all the oil and gas, the 2 degrees [Celsius] target is still possible…

3. Policy : We tested this with the Dutch Government recently – need to create an honest dialogue for a long-term perspective. Demand for energy needs to change. It’s not about supply…

[Again, some “hear hears” from the room from the Peak Oil and Peak Natural Gas deniers]

[Simon Henry] …it’s about demand. Our personal wish for [private] transport. [Not good to be] pushing the cost onto the big bad energy companies and their shareholders. It’s taxes or prices. [Politicians] must start to think of their children and not the next election…

…On targets and subsidies : India, Indonesia, Brazil […] to move on fossil fuel subsidies – can’t break the Laws of Economics forever. If our American friends drove the same cars we do, they’d reduce their oil consumption equivalent to all of the shale [Shale Gas ? Or Shale Oil ?]… Targets are an emotive issue when trying to get agreement from 190 countries. Only a few players that really matter : USA, China, EU, India – close to 70% of current emissions and maybe more in future. The EPA [Environmental Protection Agency in the United States of America] [announcement] on power emissions. China respondedin 24 hours. The EU target on 27% renewables is not [country-specific, uniform across-the-board]. Last week APEC US deal with China on emissions. They switched everything off [and banned traffic] and people saw blue sky. Coal with CCS [Carbon Capture and Storage] we see as a good idea. We would hope for a multi-party commitment [from the United Nations climate talks], but [shows doubt]… To close : a couple of words on Shell – have to do that. We have only 2% [of the energy market], but we [hope we] can punch above our weight [in policy discussions]. We’re now beginning to establish gas as a transport fuel. Brazil – low carbon [bio]fuels. Three large CCS projects in Canada, EU… We need to look at our own energy use – pretty trivial, but [also] look at helping our customers look at theirs. Working with the DRC [China]. Only by including companies such as ourselves in [climate and energy policy] debate can we get the [global deal] we aspire to…

[…]

[Question from the table, Ed Wells (?), HSBC] : Green Bonds : how can they provide some of the finance [for climate change mitigation and adaptation] ? The first Renminbi denominated Green Bond from [?]. China has committed to non-fossil fuels. The G20 has just agreed the structure on infrastructure – important – not just for jobs and growth – parallel needs on climate change. [Us at HSBC…] Are people as excited about Green Bonds as we are ?

[Stephen Tindale] Yes.

[Question from the table, Anthony Cary, Commonwealth Scholarship Commission] …The key seems to be pricing carbon into the economy. You said you preferred Cap and Trade. I used to but despite reform the EU Emissions Trading Scheme (EU ETS) – [failures and] gaming the system. Tax seems to be a much more solid basis.

[Simon Henry] [The problem with the ETS] too many credits and too many exemptions. Get rid of the exemptions. Bank reserve of credits to push the price up. Degress the number of credits [traded]. Tax : if people can afford it, they pay the tax, doesn’t stop emissions. In the US, no consumption tax, they are very sensitive to the oil price going up and down – 2 to 3 million barrels a day [swing] on 16 million barrels a day. All the political impact on the US from shale could be done in the same way on efficiency [fuel standards and smaller cars]. Green Bonds are not something on top of – investment should be financed by Green Bonds, but investment is already being done today – better to get policy right and then all investment directed.

[…]

[Question from the table, Kirsten Gogan, Energy for Humanity] The role of nuclear power. By 2050, China will have 500 gigawatts (GW) of nuclear power. Electricity is key. Particularly coal. Germany is building new coal as removing nuclear…

[My internal response] It’s at this point that my ability to swallow myths was lost. I felt like shouting, politely, across the table : ACTUALLY KIRSTEN, YOU, AND A LOT OF OTHER PEOPLE IN THE ROOM ARE JUST PLAIN WRONG ON GERMANY AND COAL.

[Kirsten Gogan]…German minister saying in public that you can’t phase out nuclear and coal at the same time. Nuclear is not included in that conversation. Need to work on policy to scale up nuclear to replace coal. Would it be useful to have a clear sectoral target on decarbonising – 100% on electricity ?

[Stephen Tindale] Electricity is the least difficult of the energy sectors to decarbonise. Therefore the focus should be on electricity. If a target would help (I’m not a fan) nuclear certainly needs to be a part of the discussions. Angela Merkel post-Fukushima has been crazy, in my opinion. If want to boost renewable energy, nuclear power will take subsidies away from that. But targets for renewable energy is the wrong objective.. If the target is keeping the climate stable then it’s worth subsidising nuclear. Subsidising is the wrong word – “risk reduction”.

[Simon Henry] If carbon was properly priced, nuclear would become economic by definition…

[My internal response] NO IT WOULDN’T. A LOT OF NUCLEAR CONSTRUCTION AND DECOMMISSIONING AND SPENT FUEL PROCESSING REQUIRES CARBON-BASED ENERGY.

[Simon Henry] …Basically, all German coal is exempted (from the EU ETS). If you have a proper market-based system then the right things will happen. The EU – hypocrisy at country level. Only [a couple of percent] of global emissions. The EU would matter if it was less hypocritical. China are more rational – long-term thinking. We worked with the DRC. Six differing carbon Cap and Trade schemes in operation to find the one that works best. They are effectively supporting renewable energy – add 15 GW each of wind and solar last year. They don’t listen to NIMBYs [they also build in the desert]. NIMBYism [reserved for] coal – because coal was built close to cities. [Relationship to Russia] – gas replacing coal. Not an accident. Five year plan. They believe in all solutions. Preferably Made in China so we can export to the rest of the world. [Their plans are for a range of aims] not just climate.

[…]

[…]

[Simon Henry] [in answer to a question about the City of London] We don’t rely on them to support our activities [my job security depends on a good relationship with them]]. We have to be successful first and develop [technological opportunities] [versus being weakened by taxes]. They can support change in technology. Financing coal may well be new money. Why should the City fund new coal investments ?

[Question from the table, asking about the “coal is 70% of the problem” message from Simon Henry] When you talk to the City investors, do you take the same message to the City ?

[Simon Henry] How much of 2.7 trillion tonnes of “Unburnable Carbon” is coal, oil and gas ? Two thirds of carbon reserves is coal. [For economic growth and] transport you need high density liquid fuels. Could make from coal [but the emissions impact would be high]. We need civil society to have a more serious [understanding] of the challenges.

After the discussion, I asked Simon Henry to clarify his words about the City of London.

[Simon Henry] We don’t use the City as a source of capital. 90% is equity finance. We don’t go to the market to raise equity. For every dollar of profit, we invest 75 cents, and pay out 25 cents as dividend to our shareholders. Reduces [problems] if we can show we can reinvest. [ $12 billion a year is dividend. ]

I asked if E&P [Exploration and Production] is working – if there are good returns on investment securing new reserves of fossil fuels – I know that the company aims for a 10 or 11 year Reserves to Production ratio (R/P) to ensure shareholder confidence.

Simon Henry mentioned the price of oil. I asked if the oil price was the only determinant on the return on investment in new E&P ?

[Simon Henry] If the oil price is $90 a barrel, that’s good. At $100 a barrel or $120 a barrel [there’s a much larger profit]. Our aim is to ensure we can survive at $70 a barrel. [On exploration] we still have a lot of things in play – not known if they are working yet… Going into the Arctic [At which point I said I hope we are not going into the Arctic]… [We are getting returns] Upstream is fine [supply of gas and oil]. Deepwater is fine. Big LNG [Liquefied Natural Gas] is fine. Shale is a challenge. Heavy Oil returns could be better – profitable, but… [On new E&P] Iraq, X-stan, [work in progress]. Downstream [refinery] has challenges on return. Future focus – gas and deepwater. [On profitability of investment – ] “Gas is fine. Deepwater is fine.”

[My summary] So, in summary, I think all of this means that Shell believes that Cap and Trade is the way to control carbon, and that the Cap and Trade cost would be borne by their customers (in the form of higher bills for energy because of the costs of buying carbon credits), so their business will not be affected. Although a Cap and Trade market could possibly cap their own market and growth as the sales envelope for carbon would be fixed, since Shell are moving into lower carbon fuels – principally Natural Gas, their own business still has room for growth. They therefore support Cap and Trade because they believe it will not affect them. WHAT THEY DON’T APPEAR TO WANT PEOPLE TO ASK IS IF A CAP AND TRADE SYSTEM WILL ACTUALLY BE EFFECTIVE IN CURBING CARBON DIOXIDE EMISSIONS. They want to be at the negotiating table. They believe that they’re not the problem – coal is. They believe that the world will continue to need high energy-dense oil for transport for some time to come. It doesn’t matter if the oil market gets constrained by natural limits to expansion because they have gas to expand with. They don’t see a problem with E&P so they believe they can keep up their R/P and stay profitable and share prices can continue to rise. As long as the oil price stays above $70 a barrel, they’re OK.

However, there was a hint in what Simon Henry talked about that all is not completely well in Petro-land.

a. Downstream profit warning

Almost in passing, Simon Henry admitted that downstream is potentially a challenge for maintaining returns on investment and profits. Downstream is petrorefinery and sales of the products. He didn’t say which end of the downstream was the issue, but oil consumption has recovered from the recent Big Dip recession, so that can’t be his problem – it must be in petrorefinery. There are a number of new regulations about fuel standards that are going to be more expensive to meet in terms of petroleum refinery – and the chemistry profiles of crude oils are changing over time – so that could also impact refinery costs.

b. Carbon disposal problem

The changing profile of crude oils being used for petrorefinery is bound to cause an excess of carbon to appear in material flows – and Simon Henry’s brief mention of petcoke is more significant than it may first appear. In future there may be way too much carbon to dispose of (petcoke is mostly carbon rejected by thermal processes to make fuels), and if Shell’s plan is to burn petcoke to make power as a solution to dispose of this carbon, then the carbon dioxide emissions profile of refineries is going to rise significantly… where’s the carbon responsiblity in that ?

This week, I had the opportunity to join the launch of the UKERC’s latest research into the future of gas. The esteemed delegates included members of a Russian Trade Delegation and several people from the US Embassy. Clearly, the future of gas is an international thing.

[MB] I’m somewhat daunted by this audience – the report is aimed perhaps for informed public audience. The media [ambushed us on the question of shale gas, shale gas attracted more attention] but things we didn’t cover much about there we can cover here. It’s been a real rollercoaster ride in the gas industry. Any flights of fancy (in the report) are our faults and not theirs [reference to work of colleagues, such as Jonathan Stern at Oxford Institute for Energy Studies]. A set of shortcomings dealing with the issue of Energy Security. There is a tendency to think that oil and gas are the same. They’re not. The framework, the actors and the networks, trade statistics, policies [much different for gas than for oil]. [In the UK for example we are seeing] a rapid increase in import dependence [and in other countries]. Need to [pay] particular understanding on what will happen in far-flung places. Today, the US-China agreement could influence gas demand. [In the literature on gas, some anomalies, perhaps]. Academics may not understand markets. [What we are seeing here is] the globalisation of UK gas security – primarily Europeanisation. There is growing uncertainty [about] the material flow of gas. [Threshold] balance in three sectors – strong seasonality, impact of climate and temperature [on gas demand]. The Russian agreement with Ukraine [and Europe] – the one thing everybody was hoping for was a warm winter. While the gas market is important [industrial use and energy use], domestic/residential demand is still very significant [proportion of total demand], so we need to look at energy efficiency [building insulation rates] and ask will people rip out their gas boilers ? For the UK, we are some way across the gas bridge – gas has enabled us to meet [most of] our Kyoto Protocol commitments. Not long until we’ve crossed it. Our coal – gone. With coal gone, what fills the gaps ? Renewable electricity – but there is much intermittency already. We’re not saying that import dependency is necessarily a problem. Physical security is not really the problem – but the [dependence on] the interconnectors, the LNG (Liquefied Natural Gas) imports – these create uncertainties. The UK also plays a role as a gas exporter – and in landing Norwegian gas [bringing it into the European market]. I’m a geographer – have to have at least one map – of gas flows [in and out of the country]. The NTS (National Transmission System – the high pressure Natural Gas-carrying pipeline network – the “backbone” of the gas transmission and distribution system of National Grid] has responded to change – for example in the increasing sources of LNG [and “backflow” and “crossflow” requirements]. There are 9 points of entry for gas into the UK at the moment. If the Bowland Shale is exploited, there could be 100s of new points of entry [the injection of biogas as biomethane into the gas grid would also create new entry points]. A new challenge to the system. [The gas network has had some time to react in the past, for example] LNG imports – the decision to ramp up the capacity was taken a long time ago. [Evolution of] prices in Asia have tracked the gas away [from the European markets] after the Fukushima Dai-ichi disaster. And recently, we have decided to “fill up the tanks” again [LNG imports have risen in the last 24 or so months]. Very little LNG is “firm” – it needs to follow the market. It’s not good to simply say that “the LNG will come” [without modelling this market]. The literature over-emphasises the physical security of the upstream supplies of gas. [The projections have] unconventional gas growing [and growing amounts of biogas]. But it’s far too early to know about shale gas – far too early to make promises about money when we don’t even have a market [yet]. Policy cannot influence the upstream especially in a privatised market. The interconnectors into the European Union means we have to pay much more attention to the Third EU Energy Package. Colleagues in Oxford are tracking that. The thorny question of storage. We have less than 5 bcm (billion cubic metres). We’d like 10% perhaps [of the winter period demand ?] Who should pay for it ? [A very large proportion of our storage is in one place] the Rough. We know what happens – we had a fire at the Rough in 2006… Everyone worries about geopolitics, but there are other potential sources of problems – our ageing infrastructure […] if there is a technical problem and high demand [at the same time]. Resilience [of our gas system is demonstrated by the fact that we have] gas-on-gas competition [in the markets] – “liquid” gas hub trading – setting the NBP (National Balancing Point). [There are actually 3 kinds of gas security to consider] (a) Security of Supply – not really a problem; (b) Security of Transport (Transit) – this depends on markets and (c) Security of Demand – [which strongly depends on whether there is a] different role for gas in the future. But we need to design enough capacity even though we may not use all of it [or not all of the time]. We have mothballed gas-fired power plants already, for reasons you all know about. We already see the failure of the ETS (European Union Emissions Trading Scheme) [but if this can be reformed, as as the Industrial Emissions Directive bites] there will be a return to gas as coal closes. The role of Carbon Capture and Storage (CCS) becomes critical in retaining gas. CCS however doesn’t answer issues of [physical energy security, since CCS requires higher levels of fuel use].

[Question from the floor] Gas has a role to play in transition. But how do we need to manage that role ? Too much focus on building Renewable Energy system. What is the impact on the current infrastructure ? For managing that decline in the incumbent system – gas is there to help – gas by design rather than gas by default.

[Question from the floor, Jonathan Stern] [In your graphs/diagrams] the Middle East is a major contributor to gas trade. We see it differently. The Qataris [could/may/will] hold back [with expanding production] until 2030. Iran – our study [sees it as] a substitute contributor. Oil-indexed gas under threat and under challenge. If you could focus more on the global gas price… [New resources of gas could be very dispersed.]Very difficult to get UK people to understand [these] impacts on the gas prices [will] come from different places than they can think of.

[Question from the floor] Availability of CCS capacity ? When ? How much ? Assumptions of cost ?

[Question from the floor : Tony Bosworth, Friends of the Earth] Gas as a bridge – how much gas do we need for [this process] ? What about unburnable carbon ? Do we need more gas to meet demands ?

[Answer – to Jonathan Stern – from Christophe McGlade ?] The model doesn’t represent particularly well political probabilities. Iran has a lot of gas – some can come online. It will bring it online if it wants to export it. Some simplifications… might be over optimistic. Your work is helpful to clarify.

On gas prices – indexation versus global gas price – all the later scenarios assumed a globalised gas price. More reasonable assumptions.

On CCS : first [coming onstream] 2025 – initially quite a low level, then increasing by 10% a year. The capital costs are approximately 60% greater than other options and causes a drop in around 10% on efficiency [because making CCS work costs you in extra fuel consumed]. If the prices of energy [including gas] increase, then CCS will have a lesser relative value [?].

On availability of gas : under the 2 degrees Celsius scenario, we could consume 5 tcm (trillion cubic metres) of gas – and this can come from reserves and resources. There are a lot of resources of Natural Gas, but some of it will be at a higher price. In the model we assume development of some new resources, with a growth in shale gas, and other unconventional gas. Because of the climate deal, we need to leave some gas underground.

[Answer from the panel] Indexation of gas prices to oil… Further gas demand is in Asia – it’s a question of whose gas gets burnt. [Something like] 70% of all Natural Gas gets burned indigenously [within the country in which it is produced]. When we talk about “unburnable gas”, we get the response “you’re dreaming” from some oil companies, “it won’t be our fossil fuels that get stranded”. LNG models envisage a different demand profile [in the future, compared to now]. When China [really gets] concerned about air quality [for example]. Different implications.

[Question from the floor, from Centrica ?] What’s in the model for the globalised gas price – Henry Hub plus a bit ? There is not a standard one price.

[Question from the floor] On the question of bridging – the long-term bridge. What issues do you see when you get to 2030 for investment ? [We can see] only for the next few years. What will investors think about that ?

[Question from the floor] [With reference to the Sankey diagram of gas use in the UK] How would that change in a scenario of [electrification – heat and transport being converted to run on electrical power] ?

[Question from the floor] Stranded assets. How the markets might react ? Can you put any numbers on it – especially in the non-CCS scenario ? When do we need to decide [major strategy] for example, [whether we could or should be] shutting off the gas grid ? How would we fund that ? Where are the pinch points ?

[Answer from the panel] On the global gas price – the model does not assume a single price – [it will differ over each] region. [The price is allowed to change regionally [but is assumed to arise from global gas trading without reference to oil prices.] Asian basin will always be more expensive. There will be a temperature differential between different hubs [since consumption is strongly correlated with seasonal change]. On stranded assets – I think you mean gas power plants ? The model is socially-optimal – all regions working towards the 2 degrees Celsius global warming target. The model doesn’t limit stranded assets – and do get in the non-CCS scenario. Build gas plants to 2025 – then used at very low load factors. Coal plants need to reduce [to zero] given that the 2 degrees Celsius targets are demanding. Will need gas for grid balancing – [new gas-fired power generation assets will be] built and not used at high load factors.

[Answer from the panel] Our report – we have assume a whole system question for transition. How successful will the Capacity Mechanism be ? UKERC looking at electrification of heating – but they have not considered the impact on gas (gas-to-power). Will the incentives in place be effective ? The Carbon Budget – what are the implications ? Need to use whole system analysis to understand the impact on gas. Issue of stranded assets : increasingly important now [not at some point in the future]. On pinch point : do we need to wait another three years [for more research] ? Researchers have looked more at what to spend – what to build – and less on how to manage the transition. UKERC have started to explore heat options. It’s a live issue. Referenced in the report.

[Question from the floor, from Richard Sverrisson, News Editor of Montel] Will reform to the EU ETS – the Market Stability Reserve (MSR) – will that be enough to bring gas plant into service ?

[Question from the floor] On oil indexation and the recent crash in the crude price – what if it keeps continuing [downwards] ? It takes gas prices down to be competitive with hub prices. [What about the impact on the economic profitability of] shale oil – where gas driving related prices ? Are there some pricing [functions/variables] in the modelling – or is it merely a physical construct ?

[Question from the floor, from Rob Gross of UCL] On intermittency and the flexibility of low carbon capacity. The geographical units in the modelling are large – the role of gas depends on how the model is constrained vis-a-vis intermittency.

[Answer from the panel, from Christophe McGlade] On carbon dioxide pricing : in the 2 degrees Celsius scenario, the price is assumed to be $200 per tonne. In the non-CCS scenario, the price is in the region of $400 – $500 per tonne [?] From 2020 : carbon price rises steeply – higher than the Carbon Floor Price. How is the the 2 degrees Celsius target introduced ? If you place a temperature constraint on the energy system, the model converts that into carbon emissions. The latest IPCC report shows that there remains an almost linear trend between carbon budget and temperature rise – or should I say a greenhouse gas budget instead : carbon dioxide (CO2), methane (CH4) and nitrous oxide (N2O). The emissions pledges of the [European Union ?] have been adopted by this model – also the development of renewable energy and fuel standards. No exogenous assumptions on carbon pricing. On intermittency – the seasonality is represented by summer, winter and intermediate; and time day generalised as morning, night, evening and peak (morning peak). [Tighter modelling would provide more] certainty which would remove ~40% of effective demand [?] Each technology has a contribution to make to peak load. Although, we assume nothing from wind power – cannot capture hour to hour market. The model does build capacity that then it doesn’t use.

[Answer from the panel] On carbon pricing and the EU ETS reform : I wouldn’t hold my breath [that this will happen, or that it will have a major impact]. We have a new commission and their priority is Poland – nothing serious will happen on carbon pricing until 2020. Their emphasis is much more on Central European issues. I don’t expect [us] to have a strong carbon price since policy [will probably be] more focussed on social democracy issues. Moving to a relatively lower price on oil : Asia will hedge. Other explorters currently sticking to indexation with oil. The low price of wet gas (condensate) in the USA is a result of the over-supply, which followed an over-supply in NGLs (Natural Gas Liquids) – a bumpy road. Implications from USA experience ? Again, comes back to watching what is happening in Asia.

It’s clear to me that the near-term and mid-term future for energy in the United Kingdom and the European Union will best be centred on Natural Gas and Renewable Electricity, and now the UK Energy Research Centre has modelled essentially the same scenario. This can become a common narrative amongst all parties – the policy people, the economists, the technologists, the non-governmental groups, as long as some key long-term de-carbonisation and energy security objectives are built into the plan.

The researchers wanted to emphasise from their report that the use of Natural Gas should not be a default option in the case that other strategies fail – they want to see a planned transition to a de-carbonised energy system using Natural Gas by design, as a bridge in that transition. Most of the people in the room found they could largely agree with this. Me, too. My only caveat was that when the researchers spoke about Gas-CCS – Natural Gas-fired power generation with Carbon Capture and Storage attached, my choice would be Gas-CCU – Natural Gas-fired power generation with Carbon Capture and Re-utilisation – carbon recycling – which will eventually lead to much lower emissions gas supply at source.

What follows is a transcription of my poorly-written notes at the meeting, so you cannot accept them as verbatim.

Jim Watson, UKERC = [JW]

Christophe McGlade, University College London (UCL) = [CM]

Mike Bradshaw, Warwick Business School = [MB]

[JW] Thanks to Matt Aylott. Live Tweeting #FutureOfGas. Clearly gas is very very important. It’s never out of the news. The media all want to talk about fracking… If we want to meet the 2 degrees Celsius target of the United Nations Framework Convention on Climate Change, how much can gas be a part of this ? Is Natural Gas a bridge – how long a ride will that gas bridge be ?

[CM] Gas as a bridge ? There is healthy debate about the Natural Gas contribution to climate change [via the carbon dioxide emissions from burning Natural Gas, and also about how much less in emissions there is from burning Natural Gas compared to burning coal]. The IPCC said that “fuel switching” from coal to gas would offer emissions benefits, but some research, notably McJeon et al. (2014) made statements that switching to Natural Gas cannot confer emissions benefits. Until recently, there have not been many disaggregated assessments on gas as a bridge. We have used TIAM-UCL. The world is divided into 16 regions. The “climate module” seeks to constrain the global temperature rise to 2 degrees Celsius. One of the outcomes from our model was that export volumes [from all countries] would be severaly impacted by maintaining the price indexation between oil and gas. [Reading from chart on the screen : exports would peak in 2040s]. Another outcome was that gas consumption is not radically affected by different gas market structures. However, the over indexation to the oil price may destroy gas export markets. Total exports of natural gas are higher under the 2 degrees Celsius scenario compared to the 4 degrees Celsius scenario – particularly LNG [Liquefied Natural Gas]. A global climate deal will support gas exports. There will be a higher gas consumption under a 2 degrees Celsius deal compared to unconstrained scenario [leading to a 4 degrees Celsius global temperature rise]. The results of our modelling indicate that gas acts as a bridge fuel out to 2035 [?] in both absolute and relative terms. There is 15% greater gas consumption in the 2 degrees Celsius global warming scenario than in the 4 degrees Celsius global warming scenario. Part of the reason is that under the 4 degrees Celsius scenario, Compressed Natural Gas vehicles are popular, but a lot less useful under the 2 degrees Celsius scenario [where hydrogen and other fuels are brought into play].

There are multiple caveats on these outcomes. The bridging period is strictly time-limited. Some sectors need to sharply reduce consumption [such as building heating by Natural Gas boilers, which can be achieved by mass insulation projects]. Coal must be curtailed, but coal-for-gas substitution alone is not sufficient. Need a convincing narrative about how coal can be curtailed. In an absence of a global binding climate deal we will get consumption increases in both coal and gas. In the model, gas is offsetting 15% of coal by 2020, and 85% by 2030. With Carbon Capture and Storage (CCS), gas’s role is drastically reduced – after 2025 dropping by 2% a year [of permitted gas use]. Not all regions of the world can use gas as a bridge. [Reading from the chart : with CCS, gas is a strong bridging fuel in the China, EU, India, Japan and South Korea regions, but without CCS, gas is only strong in China. With CCS, gas’s bridging role is good in Australasia, ODA presumably “Offical Development Assistance” countries and USA. Without CCS, gas is good for Africa, Australasia, EU, India, Japan, South Korea, ODA and USA.]

In the UK, despite the current reliance on coal, there is little scope to use it as a transition fuel. Gas is unlikely to be removed from UK energy system by 2050.

[Question from the floor] The logic of gas price indexation with the oil price ?

[CM] If maintain oil indexation, exports will reduce as countries turn more towards indigenous at-home production of gas for their domestic demand. This would not be completely counter-balanced by higher oil and therefore gas prices, which should stimulate more exports.

[Point from the floor] This assumes logical behaviour…

[Question from the floor] [Question about Carbon Capture and Storage (CCS)]

[CM] The model does anticipate more CCS – which permits some extra coal consumption [at the end of the modelling period]. Gas-CCS [gas-fired power generation with CCS attached] is always going to generate less emissions than coal-CCS [coal-fired power generation with CCS attached] – so the model prefers gas-CCS.

Amongst the chink-clink of wine glasses at yesterday evening’s Open Cities Green Sky Thinking Max Fordham event, I find myself supping a high ball orange juice with an engineer who does energy retrofits – more precisely – heat retrofits. “Yeah. Drilling holes in Grade I Listed walls for the District Heating pipework is quite nervewracking, as you can imagine. When they said they wanted to put an energy centre deep underneath the building, I asked them, “Where are you going to put the flue ?””

Our attention turns to heat metering. We discuss cases we know of where people have installed metering underground on new developments and fitted them with Internet gateways and then found that as the rest of the buildings get completed, the meter can no longer speak to the world. The problems of radio-meets-thick-concrete and radio-in-a-steel-cage. We agree that anybody installing a remote wifi type communications system on metering should be obliged in the contract to re-commission it every year.

And then we move on to shale gas. “The United States of America could become fuel-independent within ten years”, says my correspondent. I fake yawn. It really is tragic how some people believe lies that big. “There’s no way that’s going to happen !”, I assert.

“Look,” I say, (jumping over the thorny question of Albertan syncrude, which is technically Canadian, not American), “The only reason there’s been strong growth in shale gas production is because there was a huge burst in shale gas drilling, and now it’s been shown to be uneconomic, the boom has busted. Even the Energy Information Administration is not predicting strong growth in shale gas. They’re looking at growth in coalbed methane, after some years. And the Arctic.” “The Arctic ?”, chimes in Party Number 3. “Yes,” I clarify, “Brought to you in association with Canada. Shale gas is a non-starter in Europe. I always think back to the USGS. They estimate that the total resource in the whole of Europe is a whole order of magnitude, that is, ten times smaller than it is in Northern America.” “And I should have thought you couldn’t have the same kind of drilling in Europe because of the population density ?”, chips in Party Number 3. “They’re going to be drilling a lot of empty holes,” I add, “the “sweet spot” problem means they’re only likely to have good production in a few areas. And I’m not a geologist, but there’s the stratigraphy and the kind of shale we have here – it’s just not the same as in the USA.” Parties Number 2 and 3 look vaguely amenable to this line of argument. “And the problems that we think we know about are not the real problems,” I out-on-a-limbed. “The shale gas drillers will probably give up on hydraulic fracturing of low density shale formations, which will appease the environmentalists, but then they will go for drilling coal lenses and seams inside and alongside the shales, where there’s potential for high volumes of free gas just waiting to pop out. And that could cause serious problems if the pressures are high – subsidence, and so on. Even then, I cannot see how production could be very high, and it’s going to take some time for it to come on-stream…” “…about 10 years,” says Party Number 2.

“Just think about who is going for shale gas in the UK,” I ventured, “Not the big boys. They’ve stood back and let the little guys come in to drill for shale gas. I mean, BP did a bunch of onshore seismic surveys in the 1950s, after which they went drilling offshore in the North Sea, so I think that says it all, really. They know there’s not much gas on land.” There were some raised eyebrows, as if to say, well, perhaps seismic surveys are better these days, but there was agreement that shale gas will come on slowly.

“I don’t think shale gas can contribute to energy security for at least a decade,” I claimed, “even if there’s anything really there. Shale gas is not going to answer the problems of the loss of nuclear generation, or the problems of gas-fired generation becoming uneconomic because of the strong growth in renewables.” There was a nodding of heads.

“I think,” I said, “We should forget subsidies. UK plc ought to purchase a couple of CCGTS [Combined Cycle Gas Turbine electricity generation units]. That will guarantee they stay running to load balance the power grid when we need them to. Although the UK’s Capacity Mechanism plan is in line with the European Union’s plans for supporting gas-fired generation, it’s not achieving anything yet.” I added that we needed to continue building as much wind power as possible, as it’s quick to put in place. I quite liked my radical little proposal for energy security, and the people I was talking with did not object.

There was some discussion about Green Party policy on the ownership of energy utilities, and how energy and transport networks are basically in the hands of the State, but then Party Number 2 said, “What we really need is consistency of policy. We need an Energy Bill that doesn’t get gutted by a change of administration. I might need to vote Conservative, because Labour would mess around with policy.” “I don’t know,” I said, “it’s going to get messed with whoever is in power. All those people at DECC working on the Electricity Market Reform – they all disappeared. Says something, doesn’t it ?”

I spoke to Parties Number 2 and 3 about my research into the potential for low carbon gas. “Basically, making gas as a kind of energy storage ?”, queried Party Number 2. I agreed, but omitted to tell him about Germany’s Power-to-Gas Strategy. We agreed that it would be at least a decade before much could come of these technologies, so it wouldn’t contribute immediately to energy security. “But then,” I said, “We have to look at the other end of this transition, and how the big gas producers are going to move towards Renewable Gas. They could be making decisions now that make more of the gas they get out of the ground. They have all the know-how to build kit to make use of the carbon dioxide that is often present in sour conventional reserves, and turn it into fuel, by reacting it with Renewable Hydrogen. If they did that, they could be building sustainability into their business models, as they could transition to making Renewable Gas as the Natural Gas runs down.”

I asked Parties Number 2 and 3 who they thought would be the first movers on Renewable Gas. We agreed that companies such as GE, Siemens, Alstom, the big engineering groups, who are building gas turbines that are tolerant to a mix of gases, are in prime position to develop closed-loop Renewable Gas systems for power generation – recycling the carbon dioxide. But it will probably take the influence of the shareholders of companies like BP, who will be arguing for evidence that BP are not going to go out of business owing to fossil fuel depletion, to roll out Renewable Gas widely. “We’ve all got our pensions invested in them”, admitted Party Number 2, arguing for BP to gain the ability to sustain itself as well as the planet.

Sigh. I think I’m going to need to start sending out Freedom of Information requests… Several cups of tea later…

To: Information Rights Unit, Department for Business, Innovation & Skills, 5th Floor, Victoria 3, 1 Victoria Street, London SW1H OET

28th April 2014

Request to the Department of Energy and Climate Change

Re: Policy and Strategy for North Sea Natural Gas Fields Depletion

Dear Madam / Sir,

I researching the history of the development of the gas industry in the United Kingdom, and some of the parallel evolution of the industry in the United States of America and mainland Europe.

In looking at the period of the mid- to late- 1960s, and the British decision to transition from manufactured gas to Natural Gas supplies, I have been able to answer some of my questions, but not all of them, so far.

From a variety of sources, I have been able to determine that there were contingency plans to provide substitutes for Natural Gas, either to solve technical problems in the grid conversion away from town gas, or to compensate should North Sea Natural Gas production growth be sluggish, or demand growth higher than anticipated.

Technologies included the enriching of “lean” hydrogen-rich synthesis gas (reformed from a range of light hydrocarbons, by-products of the petroleum refining industry); Synthetic Natural Gas (SNG) and methane-“rich” gas making processes; and simple mixtures of light hydrocarbons with air.

In the National Archives Cmd/Cmnd/Command document 3438 “Fuel Policy. Presented to Parliament by the Minister of Power Nov 1967”, I found discussion on how North Sea gas fields could best be exploited, and about expected depletion rates, and that this could promote further exploration and discovery.

In a range of books and papers of the time, I have found some discussion about options to increase imports of Natural Gas, either by the shipping of Liquified Natural Gas (LNG) or by pipeline from The Netherlands.

Current British policy in respect of Natural Gas supplies appears to rest on “pipeline diplomacy”, ensuring imports through continued co-operation with partner supplier countries and international organisations.

I remain unclear about what official technological or structural strategy may exist to bridge the gap between depleting North Sea Natural Gas supplies and continued strong demand, in the event of failure of this policy.

It is clear from my research into early gas field development that depletion is inevitable, and that although some production can be restored with various techniques, that eventually wells become uneconomic, no matter what the size of the original gas field.

To my mind, it seems unthinkable that the depletion of the North Sea gas fields was unanticipated, and yet I have yet to find comprehensive policy statements that cover this eventuality and answer its needs.

Under the Freedom of Information Act (2000), I am requesting information to answer the following questions :-

1. At the time of European exploration for Natural Gas in the period 1948 to 1965, and the British conversion from manufactured gas to Natural Gas, in the period 1966 to 1977, what was HM Government’s policy to compensate for the eventual depletion of the North Sea gas fields ?

2. What negotiations and agreements were made between HM Government and the nationalised gas industry between 1948 and 1986; and between HM Government and the privatised gas industry between 1986 and today regarding the projections of decline in gas production from the UK Continental Shelf, and any compensating strategy, such as the development of unconventional gas resources, such as shale gas ?