|

“Britain must not miss out on fracking: Cameron says drilling for shale gas should take place at more sites : PM said it would be ‘big mistake if Government did not encourage fracking : Wants to dispel ‘myths’ that drilling for gas leads to earthquakes : By Tim Shipman and Nazia Parveen : PUBLISHED: 00:45, 9 August 2013 : David Cameron warned last night that Britain was ‘missing out big time’ on the benefits of fracking by not drilling at enough sites in the search for shale gas. In his most outspoken comments about the technology, the Prime Minister said it would be a ‘big mistake’ if the Government did not encourage fracking across Britain. Mr Cameron said the Government would dispel ‘myths’ from green groups that drilling for gas would lead to earthquakes, and he dismissed fears that it could lead to water taps catching fire. But campaigners last night accused him of lying about the dangers, as he suggested the UK should copy the US, where thousands of wells have been bored […]”

What are these purported benefits of shale gas, then ? Apparently, drilling for shale gas may bring gas prices down, by comparison with the American experience :-

https://www.telegraph.co.uk/finance/newsbysector/energy/10186007/Gas-prices-could-fall-by-a-quarter-with-shale-drilling-Government-advisers-say.html

“Gas prices could fall by a quarter with shale drilling, Government advisers say : Gas prices could fall by a quarter and help bring down household energy bills if Britain exploits its shale gas reserves, a report commissioned by Ed Davey, the Energy Secretary, suggests. : By Rowena Mason, Political Correspondent : 5:08PM BST 17 Jul 2013 : The study by Navigant Consulting backs up David Cameron’s claim that shale gas drilling could help cut the cost of living for families struggling with average bills of more than £1,300 per year. However, it contrasts with the claims of Ed Davey, the Energy Secretary, that shale gas is “unlikely” to bring down household bills. He has said higher gas prices are probable regardless of the discovery of Britain’s shale reserves and used this argument to justify spending billions on wind farms and nuclear power stations. […]”

OK, let’s do a propaganda scan and a fact check.

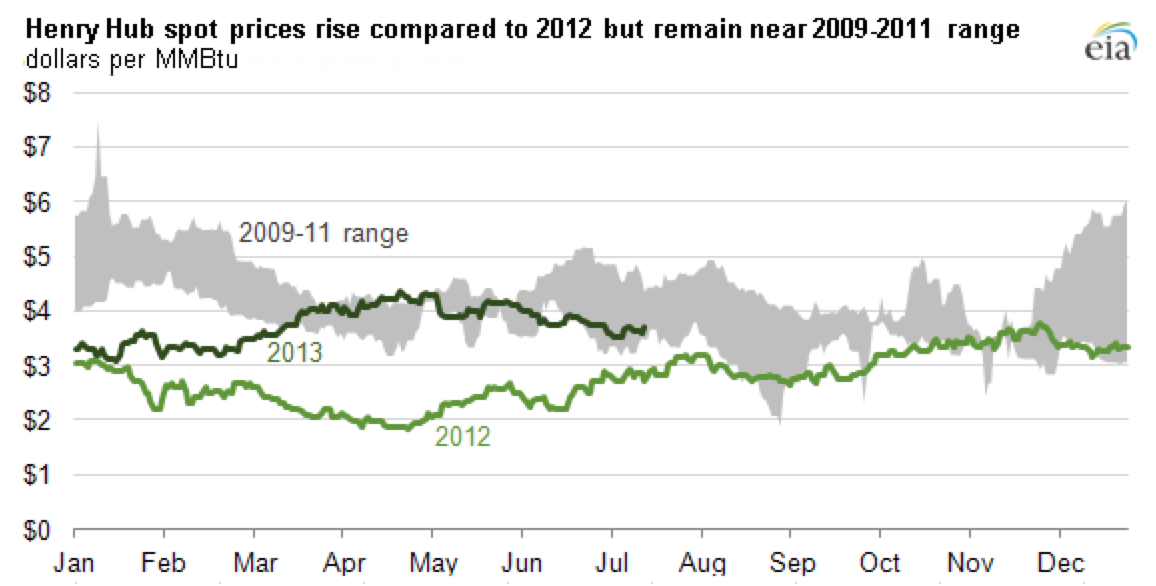

Meme #1 : American Natural Gas prices have dropped because of shale gas drilling.

Fact #1 : American Natural Gas prices have risen during 2013.

https://www.eia.gov/todayinenergy/detail.cfm?id=12191

Fact #2 : American Natural Gas prices have been tied to oil prices. Take away the oil-price related spikes of the last 20 years, and Natural Gas prices have stayed fairly constant :-

https://www.eia.gov/dnav/ng/hist/rngwhhdm.htm

Fact #3 : The cost of drilling natural gas wells has risen sharply :-

https://www.eia.gov/dnav/ng/hist/e_ertwg_xwwn_nus_mdwa.htm

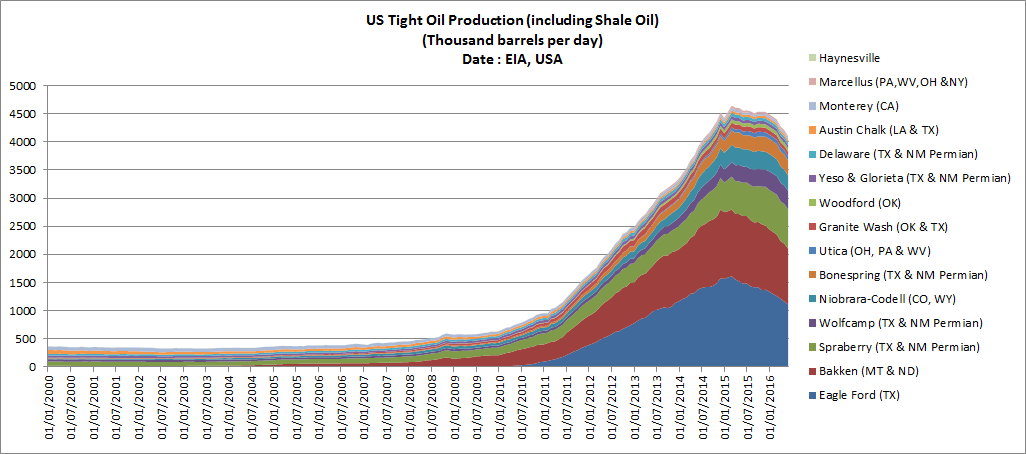

Fact #4 : A boom in Natural Gas well drilling has come to an end :-

https://www.eia.gov/dnav/ng/hist/e_ertwg_xwwn_nus_mdwa.htm

https://www.eia.gov/dnav/ng/hist/e_ertrrg_xr0_nus_cm.htm

Conclusion : It appears that the rise in shale gas production and the lowering of American Natural Gas prices are strongly correlated to the well-drilling boom that ended around about 2008.

Meme #2 : Natural Gas is displacing coal

Fact #1 : It did while the drilling boom was in full swing. Not now :-

https://www.eia.gov/todayinenergy/detail.cfm?id=11391

Meme #3 : Shale Gas production is going to contribute significantly more to overall Natural Gas production in the next decades.

Question #1 : Not necessarily :-

https://www.indianagasification.com/benefits/energy-benefits/shift-in-drilling-activity/

https://www.roperld.com/science/minerals/shalegas.htm

https://www.silverbearcafe.com/private/09.12/shalegas.html

https://www.newscientist.com/article/dn23968-frack-on-or-frack-off-can-shale-gas-save-the-planet.html

The Future of Fracking

Frack on or frack off: Can shale gas save the planet?

08 August 2013 by Michael Brooks

Magazine issue 2929.

Optimists see the new resource as a cheap, clean “bridging fuel” to a low-carbon future.

The true picture might not be so simple

IT’S all right. Everything’s going to be OK. If there’s a problem, we’ll fix it.

Such reassuring words are the hallmark of a certain way of thinking, sometimes known as rational optimism. Things will always turn out fine because we humans are almost infinitely creative and adaptable. Confronted with a problem, our technological ingenuity will provide a solution.

In few places is this idea more powerful than among those planning our future energy supply. Yes, demand is rising. Yes, there are issues with greenhouse gas emissions. Yes, renewable technologies aren’t quite ready for prime time. But a technological miracle will fill the gap until solar, wind and tidal power come fully on stream. It’s called shale gas.

At first glance, it is a strange claim. Shale gas is methane trapped in tiny pockets in shale rock formations, sometimes in vast quantities. Forcibly extracted by the process of hydraulic fracturing, or fracking, it is still a fossil fuel; burning methane produces greenhouse gases that contribute to global warming.

But to see the optimists’ point, look to what has happened in the US, traditionally the global climate bogeyman. Between 1981 and 2005, US carbon emissions increased by 33 per cent, from 4.5 billion to 6 billion tonnes a year. Since 2005, they have fallen by 9 per cent (see graph). There are many factors, not least economic recession, but according to figures from the US Energy Information Administration (EIA) just under half of that reduction is down to one thing: shale gas. Replicate that success globally, and we might begin to solve the emissions problem without rushing into an ill-thought-out renewables revolution, say the enthusiasts. Shale gas is technology’s answer to the climate problem, a “bridging fuel” to a cleaner, greener future. The burning question is: are the optimists right?

There is no doubt that we need to clean up our ways of generating energy, and fast. In the West, we think of coal as a fuel in terminal decline. Globally, we have never burned more. According to the International Energy Agency (IEA), coal provides 40 per cent of the world’s electricity, and could surpass oil as the world’s primary source of energy by 2017. As we exploit the cheapest sources we can find, coal is also getting dirtier. It now produces more than twice the carbon dioxide emissions of natural gas – and a lot more soot, radioactive ash, oxides of nitrogen, sulphur dioxide and other pollutants besides. Not least because of our appetite for coal, global emissions of greenhouse gases continue to rise relentlessly.

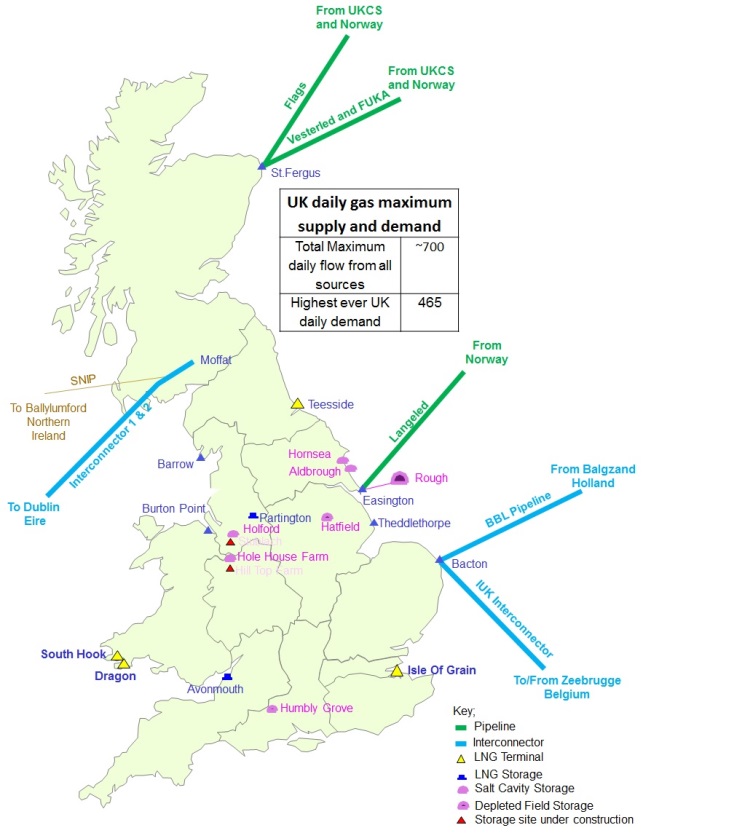

Shale gas represents a new source of natural methane gas perfectly placed to displace coal in power stations. Shale rocks are found throughout the world, formed when mud is slowly crushed so that particles of clay, quartz, calcite and other minerals end up loosely held together. The Canadian Rockies have the Burgess shale, laid down in the Cambrian era some 500 million years ago and famed for the insights into evolution given by the fossils preserved there. The UK has the 315-million-year-old Bowland shale in the north of England, and other formations dotted around. The US is riddled with different formations, among them the Barnett shale in Texas, which dates back some 350 million years, and the 400-million-year-old Marcellus shales of the Appalachians (see map).

All of these shales have one thing in common: the tiny gaps between their particles provide pockets where both oil and methane gas can happily sit undisturbed for millions of years. Fracking involves drilling into these pockets and pumping a liquid down at high pressure to break up the shale and release the stored hydrocarbons. Oil and gas escape via a central pipe to the surface where they are collected and shipped off, the methane to be burned just like conventional natural gas in homes and power stations.

Fracking has been used to extract “tight” gas trapped in highly impermeable rock formations in the US for a couple of decades now. Shale-gas extraction has been slower to get going. “The US shale gas sector took 25 to 30 years to get to where it is now,” says Joseph Dutton, who researches energy policy at the University of Leicester, UK. The first big field to be exploited was the Texan Barnett shale starting in the late 1990s. More followed, including the vast Marcellus shale that stretches from New York state through Pennsylvania and West Virginia into Ohio.

But it is only in the past five years, with innovations such as horizontal drilling, that fracking has really taken off. Here the initial vertical shaft into the shale becomes a hub for radiating spokes, sometimes kilometres long, running parallel to the surface. This allows vast volumes of shale to be exploited while causing minimal disruption at the surface. “You can have an area the size of a small parking lot, and drill 16 wells all splaying out from the same location,” says Richard Davies of the Durham Energy Institute in the UK. Thanks to such techniques, the US now has the most productive shale gas fields in the world, contributing over a third of its natural gas supply (see diagram).

As a result, shale gas is now cheaper than coal in the US, and is rapidly displacing it for electricity generation. With its vast supplies of shale gas and oil, the US could become self-sufficient in energy by 2035, according to the EIA. With labour costs in China set to rise over the same time, for many ambitious US politicians this cheap energy is nothing less than a chance for the US to regain its status as the world’s manufacturing and economic powerhouse – while getting greener too.

Small wonder other countries around the world would like to pull off a similar trick. China is one. The world’s largest producer and consumer of coal, in 2010 it covered 70 per cent of its energy needs with well over 3 billion tonnes of the stuff – almost as much as the rest of the world combined. It is now the world’s top CO2 emitter. By happy coincidence, it is also thought to be sitting on the world’s largest reserves of shale gas – over 30 trillion cubic metres. That’s 50 per cent more than the US and 12 times greater than China’s conventional gas resources. Using even a fraction of that to displace coal would make a huge difference to global emissions.

So keen is China that it is even breaking with precedent and calling on Western expertise to help kick-start production, says Julio Friedmann, an energy expert at the Lawrence Livermore National Laboratory in California. An agreement between Shell and the state-controlled PetroChina, for example, will see Shell spending $1 billion a year to help recover shale gas from 3500 square kilometres in the Sichuan basin in central China.

In the UK, a couple of exploratory fracking sites are up and running, and the government recently announced generous subsidies for would-be frackers. In its World Energy Outlook, the IEA predicts that more than a million shale gas wells could be drilled worldwide by 2035.

Not everyone is happy. Opponents across the world point out that fracking destabilises the ground (see “Earth movers”), and that the chemicals pumped into the ground during fracking can leak out, perhaps contaminating groundwater (see “Water worries”).

Supporters argue that such concerns are overblown. And in global terms, given the urgency of the climate situation, the size of shale gas reserves and the slow pace of development on renewables, it is understandable why so many people are keen to override objections. Even some green groups say shale gas makes sense as a “coal killer” – a cheaper, greener electricity generating solution. Perhaps it obviates the need to develop alternative energies entirely. “For some people, gas is not only the bridge to the future – it is the future,” says Jim Watson of the UK Energy Research Centre in London. But are things that simple?

A complex space

Let’s start with the economics. Shale gas is very cheap right now, so heady predictions are being made when its price and cost are in “disequilibrium”, says energy economist Francis O’Sullivan of the Massachusetts Institute of Technology. Shale gas was developed in the US when conventional sources of oil and gas were drying up, so shale gas could command a decent price. As fracking technology matured, productivity rose and the price fell. In fact, it has fallen so low that many companies are only continuing with production to keep a stake in the market. The productivity of the wells also falls over time: the more gas you get out of a well, the more pressure you have to apply to keep the flow coming, and there are limits to the pressure you can generate. All this means that higher prices will make a comeback once the first wave of exploitation is over, says O’Sullivan. The EIA projects that the price of natural gas, including shale gas, will double over the next 20 years. “People need to look beyond what the price has been for the last six months. This is a very complex space,” says O’Sullivan.

And even if the US shale-gas revolution is more than a flash in the pan, there is no guarantee that its success can be replicated elsewhere. There are the poorly understood vagaries of geology, for a start. Every shale in the world is different. The Barnett shale is a flat, solid expanse, whereas shales in the UK and China tend to be more fragmented, existing as a peppering between other types of rock. Hitting such a shale with a fracking drill is not straightforward. And different shales have different origins: marine-deposited rock, which is the predominant form in the Texan Barnett shale, contains almost twice as much organic material as deposits that come from land-based plants and organisms, so should be richer in gas.

In the case of the UK, it is not yet clear whether or not the shales are likely to yield much worth burning. The government-sponsored British Geological Survey (BGS) and others are currently working to assess the size of the national reserves. Last month they released a report estimating that the Bowland shale contains something between 23 and 65 trillion cubic metres of “gas in place”, doubling previous estimates. Most of that gas will never see the light of day: not all shales are brittle enough to fracture under pressure, and not all gas can be extracted using feasible pressures. Usually less than 10 per cent of gas in place is a recoverable reserve of the sort that the EIA and others base their figures on. Different layers of shale will contain different amounts of recoverable gas. “The key question is which layers in our thick shales will yield good gas,” says Michael Stephenson of the BGS. In particular it would be good to know which, if any, contain evidence of bacterial or algal matter likely to make them a good source of hydrocarbons. “We need a way of predicting where these sweet spots will be, but at the moment we don’t have that nailed down,” says Stephenson. Until that happens, any shale-gas revolution in the UK remains a pipe dream.

In Poland, things have proved particularly frustrating. The country has perhaps the largest shale gas reserves in Europe, but for reasons no one quite understands, fracking there has released negligible amounts of methane, leaving even Texan experts scratching their heads. “Some companies have left already,” Stephenson says. “But it wasn’t easy in Texas either, at the beginning.”

Not so rosy

So no one should bank on shale gas coming at all, and certainly not on it coming cheap. “It’s dangerous when people try to build policy based on low pricing that is not going to be sustainable,” says O’Sullivan. The head of the IEA, Maria van der Hoeven, has recently warned that geology and economics mean that other countries are unlikely to replicate the US’s shale-gas boom.

Leaving local environmental concerns aside, the global environmental picture of shale gas may well not be so rosy, either. One hotly debated issue is the amount of methane, a potent greenhouse gas, that escapes into the atmosphere during fracking. Such escapes are generally not included in point-of-use emissions comparisons with coal (see “Gas alert”).

More insidious, though, are the knock-on effects of shale gas on world energy markets. The US shale-gas revolution has not stopped coal being burned, but merely shifted where it is burned. Cheap gas has led to a surfeit of US coal that is now being greedily consumed elsewhere. In 2012, US coal exports reached a record 104 million tonnes, 70 per cent to Europe. Contrary to perceptions of a “dash for gas”, the UK’s consumption of coal increased by over 30 per cent in 2012, according to government figures, with gas generation falling by a comparable amount (see graph). Despite near-zero economic growth, the UK’s total carbon emissions rose by 3.5 per cent in 2012, “primarily from lower use of gas and greater use of coal for electricity generation at power stations”, a government report made plain.

Having decided to abandon nuclear power, Germany needs to generate more electricity in the short term from fossil-fuel sources, and has similarly been liberally helping itself to US coal. Where coal is cheaper than gas, energy companies will always choose the dirty option. With the jury out on whether any European country has any economically or technologically viable shale gas reserves, this impact on emissions is likely to continue in the short to medium term. If and when shale gas does come on stream, its depressing effect on the price of coal will probably lead to more coal being burned elsewhere.

But it is in China that the global emissions trajectory will be decided over the coming decades. Here, it seems unlikely that shale gas will have much impact, either. “Coal will still be much cheaper than the estimates of how much [Chinese] shale gas is going to cost,” says Sergey Paltsev, an energy economist at MIT. A significant factor is that China’s shale-gas reserves are in precisely the wrong place: in mountainous, earthquake-prone Sichuan and the water-starved desert of Xinjiang in the north-west of the country, far away from big population centres. “Transport costs and infrastructure requirements are likely to add at least another 50 per cent to the cost of gas to consumers in major urban areas,” says Paltsev.

“There isn’t going to be a wholesale swap of coal for gas,” says Friedmann. China still plans to build another 400,000 megawatts of coal-powered electricity generation over the next decade or so. Given coal’s cheapness, Friedmann doubts that China will use shale gas for power generation at all, predicting that it will instead be used to provide “high value” products such as fertiliser, district heating and transport fuel. The impact on the country’s environmental balance is likely to be limited. “I believe it’s possible to reduce Chinese emissions by 100 to 150 million tonnes a year by 2020 or 2025,” says Friedmann. “In a country that’s emitting 8 billion tonnes of CO2 per year, that’s not quite what we’d like.”

So, frack on or frack off, in both local and global terms, environmentally and economically, shale gas is unlikely to be a magic bullet. Used wisely, it could be part of the climate solution. But in the real world, economics and energy policies being what they are, its emissions will come in addition to coal’s, not instead of them. In the crucial coming decades when we need to begin reducing emissions fast, that is no help at all. “All these issues mean the urgency around climate change persists,” says Friedmann.

For Paltsev, the worry is that, seduced by a false promise of cheap, plentiful energy from shale gas, we will cut back on investment in truly green, renewable alternatives. If so, as the costs and emissions associated with shale gas rise in the future, as they inevitably will, we will end up on a costly bridge to nowhere. To see shale gas as a solution is certainly optimistic; whether it is entirely rational is quite another question.

Earth movers

To opponents of fracking, nothing symbolises its dangers and uncertainties more than its seismic potential. The issue hit the headlines in the UK in 2011 following tremors of magnitude 1.5 and 2.3 that were felt around an exploratory fracking site near Blackpool in the north-west of the country.

There is little doubt fracking caused the quakes, as reports commissioned by Cuadrilla Resources, the company involved, and the UK government concluded. Anything else would be a surprise, says Joseph Dutton of the University of Leicester, UK. “You’re taking something out of the ground so something’s going to shift – that’s basic geology.”

Should we be worried? Richard Davies of the Durham Energy Institute in the UK and his colleagues have analysed 198 instances of seismic activity of over magnitude 1.0 induced by human activity since 1929. Causes are varied: mining, oil-field depletion, filling reservoirs with water, injecting water into the ground for geothermal power, waste disposal, atomic bomb tests.

Fracking is directly implicated in two instances, one of them being the Blackpool events, and another three resulted from fracking wastewater disposal. The largest of these, in the Horn river basin in Canada in 2011, was of magnitude 3.8, but it was barely detectable by people on the surface.

By comparison, the impoundment of water in reservoirs has caused 39 earthquakes of magnitude up to 7.8. Even if fracking is a relatively new technology, the evidence suggests that seismicity is not a prime concern. “Earthquake is a wonderful word: it induces visions of a disaster movie,” says Dutton. “But the debate about seismic activity has got out of control.”

Water worries

The water used in fracking contains sand to prop open cracks, lubricants to get the sand into those cracks, biocide to make sure bugs do not clog up the pipes, and hydrochloric acid to dissolve excess cement in the pipe bore and parts of the fracked rock. About 20 per cent of this chemical cocktail does not remain in the ground, but flows back to the surface carrying heavy metals and radioactive elements flushed out of the rock. In most US states this water can be treated in standard wastewater plants, but the safety of this practice has been questioned. The state government of Pennsylvania, which sits on the large Marcellus shale formation, has banned it.

But could toxic chemicals from fracking leach into groundwater and reach reservoirs and drinking water supplies underground? So far, the indications from studies by Robert Jackson and colleagues at Duke University in Durham, North Carolina, are that the risks are low. “We have not found evidence of the fracking chemicals that people are most concerned about, such as benzene, and we have not found evidence for metal salts from deep underground,” he says.

Their studies have, however, found an issue with methane contamination in water drawn from within a kilometre or two of some wells. “It may be that the high volumes and high pressures used in fracking make leaky wells more likely,” says Jackson. He suggests a variety of regulatory measures to avoid this problem, such as stricter building codes for wells and increased minimum distances between wells and groundwater sources. The US Environmental Protection Agency is carrying out an investigation of the effect of fracking on drinking water, due out next year. The arguments will continue at least until then.

Gas alert

One problem with shale gas is very much up in the air: leaks of the potent greenhouse gas methane. “It’s much more powerful than carbon dioxide – 25 to 30 times more, molecule for molecule,” says Robert Jackson of Duke University in Durham, North Carolina.

While he and his colleagues have found evidence of direct methane leaks from a small proportion of hundreds of wells they investigated, Jackson sees them as symptoms of poor construction and ineffective regulation, and therefore potentially curable.

Not everyone is so bullish. Robert Howarth of Cornell University in Ithaca, New York, points out that methane is also released from the “flowback” water that returns to the surface during the fracking process. Working with figures from the US Environmental Protection Agency and General Accountability Office, Howarth and his colleagues have calculated that between 4 and 8 per cent of a well’s total production of methane goes straight into the atmosphere. Such a methane release creates an increased greenhouse gas burden of between 20 and 100 per cent over coal for the first 20 years of a field’s exploitation. “Shale gas is not a suitable bridge fuel for the 21st century,” they conclude.

That analysis is highly controversial. Lawrence Cathles, also at Cornell, points out that the 20-year timescale biases things against shale gas because methane has a much shorter lifetime in the atmosphere than CO2. Emissions from coal will have longer effect. Francis O’Sullivan and Sergey Paltsev of MIT have calculated that the practice of “flaring” – burning off methane for a few weeks while a well is established – brings the greenhouse-gas footprint of shale gas back down in line with that of natural gas, and much better than coal’s.

Jackson’s analysis suggests that, rather than worrying about emissions from fracking itself, we should concentrate on leakages downstream in the supply chain. “In Boston alone we found 3000 methane leaks from pipelines,” he says. Fixing those problems is more easy than fixing the emission problems of coal.

Michael Brooks is a New Scientist consultant. His latest book is The Secret Anarchy of Science (Profile/Overlook)

This article appeared in print under the headline “Frack to the future”

Issue 2929 of New Scientist magazine

From issue 2929 of New Scientist magazine, page 36-41.

EDITORIAL

https://www.newscientist.com/article/mg21929291.700-the-fracking-debate-needs-more-light-less-heat.html

The fracking debate needs more light, less heat

07 August 2013

Magazine issue 2929.

DEBATES over fracking tend to generate more heat than light.

Nowhere is that more true than in the UK, where the past week has seen a former government energy adviser suggest that the practice should be confined to the “desolate” north-east, even as vociferous protests erupted near a normally tranquil village in the prosperous Home Counties.

Safety concerns over fracking are overblown – but so are the boosterish claims made for its environmental and economic benefits (see “Fracking could accelerate global warming” and “Frack on or frack off: Can shale gas really save the planet?”). The British Geological Survey has so far assessed only the Bowland shale in the north of England, concluding that there is perhaps twice as much “gas in place” as previously thought. But it remains to be seen if this gas is recoverable or good for burning.

So drill and find out, say advocates. Not in my backyard, say protesters. Enough. Neither nimbyism nor bravado is appropriate given what we know about the risks and rewards of fracking. Better to bring that vigour to bear on a wider debate aimed at shedding light on the nature of a truly sustainable energy policy for the UK – and, for that matter, the world.

This article appeared in print under the headline “More light, less heat”

Issue 2929 of New Scientist magazine

From issue 2929 of New Scientist magazine, page 5.

https://www.newscientist.com/article/mg21929292.000-fracking-could-accelerate-global-warming.html

Fracking could accelerate global warming

07 August 2013

Magazine issue 2929. Subscribe and save

Editorial: “The fracking debate needs more light, less heat”

THE row over fracking for natural gas has hit the UK, with protests over plans in the village of Balcombe. Could they have a point? Studies are suggesting fracking could accelerate climate change, rather than slow it.

The case for fracking rests on its reputed ability to stem global warming. Burning gas emits half as much planet-warming carbon dioxide as an equivalent amount of coal. That is why, after embracing fracking, CO2 emissions have fallen in the US.

But leading climate scientists are warning that this benefit is illusory. Tom Wigley of the National Center for Atmospheric Research in Boulder, Colorado, concluded in a recent study that substituting gas for coal increases rather than decreases the rate of warming for many decades (Climatic Change, doi.org/dv4kbp).

Firstly, burning coal releases a lot of sulphur dioxide and black carbon. These cool the climate, offsetting up to 40 per cent of the warming effect of burning coal, Wigley told a recent conference of the Breakthrough Institute think tank in Sausalito, California.

Fracking technology, which involves pumping water at high pressure into shale beds to release trapped gas, also leaks methane into the atmosphere. Methane is a much more potent greenhouse gas than CO2 and Wigley says that switching from coal to gas could only bring benefits this century if leakage rates get below 2 per cent. If rates are at 10 per cent – the top end of current US estimates – the gas would deliver extra warming until the mid-22nd century.

A recent review by the UN Environment Programme agreed that emissions from fracking and other unconventional sources of natural gas could boost warming initially, and would only be comparable to coal over a 100-year timescale.

This article appeared in print under the headline “Frack for warming”

Issue 2929 of New Scientist magazine

From issue 2929 of New Scientist magazine, page 6.

|

{kind=link}

{kind=link}

{kind=link}

{kind=link}